PayTo is the highly anticipated new real-time pull payment service from New Payments Platform Australia (NPPA). It will allow businesses and merchants to initiate real-time payments from their customers' bank accounts while giving customers greater visibility and control over their payments via an enhanced digital experience.

Zai sat down with Katrina Stuart, Head of Engagement with NPPA, to discuss the genesis and development of PayTo, the benefits it brings to both businesses and consumers and how it will be rolled out.

Along the way we gleaned some fascinating insights into a service that will play a huge role in the Australian payments market in the future.

Describe how the concept of PayTo came into existence?

We started working with the industry to look at “debit like” capability even before the New Payments Platform (NPP) went live in early 2018. The intention was always for the platform to support debit like payments in addition to the current credit payment that is available on the NPP (whereby I have to “push” a payment from my bank account).

Initially, we were focused on designing a better alternative to direct debit in the market that addressed some of the pain points that exist today. However, as we further developed the capability, one of our key principles was to design it in such a way that it could be broad and extendable. We wanted to be able to build it once but reuse it for several purposes rather than having to come back in a few years’ time and build something else.

This means the service has been designed to support a broad range of use cases from recurring payments to linking a bank account for in-app payments, “account-on-file” type arrangements for e-commerce and subscription services, funding for other payment options like digital wallets and buy now, pay later services, and for one-off payments.

Businesses can also use it to enable third parties to conduct payments on their behalf, such as corporate payroll and accounts payable. Given the likely extension of the Consumer Data Right (CDR) in Australia (our version of Open Banking) it was also intentionally designed to provide a broad and scalable solution for third party payment initiation.

How did you decide on the name, PayTo?

The initial name for the service was Mandated Payments Service but this was always intended to be just an industry working title.

In 2020 we engaged an agency to help us work through the process of finding a suitable name. We had a set of criteria that guided us including being trademarkable, being descriptive and functional (“it needed to do what it says on the tin”), familiar and easy to remember, and it needed to fit alongside PayID, our other market facing brand for our alias addressing service. Early on in the process we decided that having “Pay” in the name worked well given our role in the payments system and the fact that we are all about payments.

We developed a short list and tested various options but none of those initial options resonated. So we went back to the drawing board and created a new short list that honed in on five options. We began the trademark process and in parallel tested our options in focus groups - and finally from an initial list of 350 options, out popped “PayTo”.

We’re really happy with the final result and feel that it works well. We also developed a stylised wordmark so it will be instantly recognisable to people. For anyone wanting to know a bit more, we recently recorded a short podcast on the selection of the PayTo name which can be listened to here.

What pain points does PayTo solve for both the payer and the payee?

For payers, PayTo provides more visibility and control over payments from their bank account. They can see all PayTo agreements that they have authorised in one place, within their internet or mobile banking. They can cancel, pause and resume those agreements and make certain amendments. Given PayTo agreements are authorised within the safety and security of a payer customer’s banking channel, they are also seen as a safer way to pay. Customers can also choose to use either their PayID or BSB and account number, making it easy to set up PayTo agreements.

For payees or third parties looking to initiate payments, there are a number of benefits including real-time account validation when a PayTo agreement is created; real-time funds verification at the time of payments; notifications when a PayTo agreement is paused, changed or cancelled; easier reconciliation with the additional information that can be contained in PayTo agreements; support APIs to deliver more seamless and efficient processes; and centralised, secure storage of PayTo agreements which are readily accessible.

One of the other key benefits is that third parties only need one access point if they want to use PayTo to initiate and receive payments from all eligible NPP accounts. So regardless of where the payer customer holds their bank account, if its NPP enabled and can make “debit like” payments, it can be reached via that one integration point. That’s a huge efficiency gain for organisations wanting to use the service.

Use cases that are supported are recurring payments, e-commerce and in-app payments, using your bank account as a funding source for other payment solutions such as digital wallets and buy now, pay later (BNPL) solutions, for “on behalf of” payments such as corporate payroll, accounts payable and e-invoicing and together with QR codes.

How are you collaborating with payment providers?

As operator of the real-time payments infrastructure and the PayTo service, our role is to provide the market, including payment providers, information about the service so they can start to work through how they may use it for their own specific needs and incorporate it into their payment service offerings and solutions. So that means information on how the service works technically, what the customer experience (CX) looks like, what access options they have, brand and marketing guidelines and access to our marketing collateral.

As delivery of the service gets closer, we will actively support early adopter organisations who will be the first to use the service to initiate payments from customers' bank accounts.

What will a payer and a payee customer journey look like for PayTo?

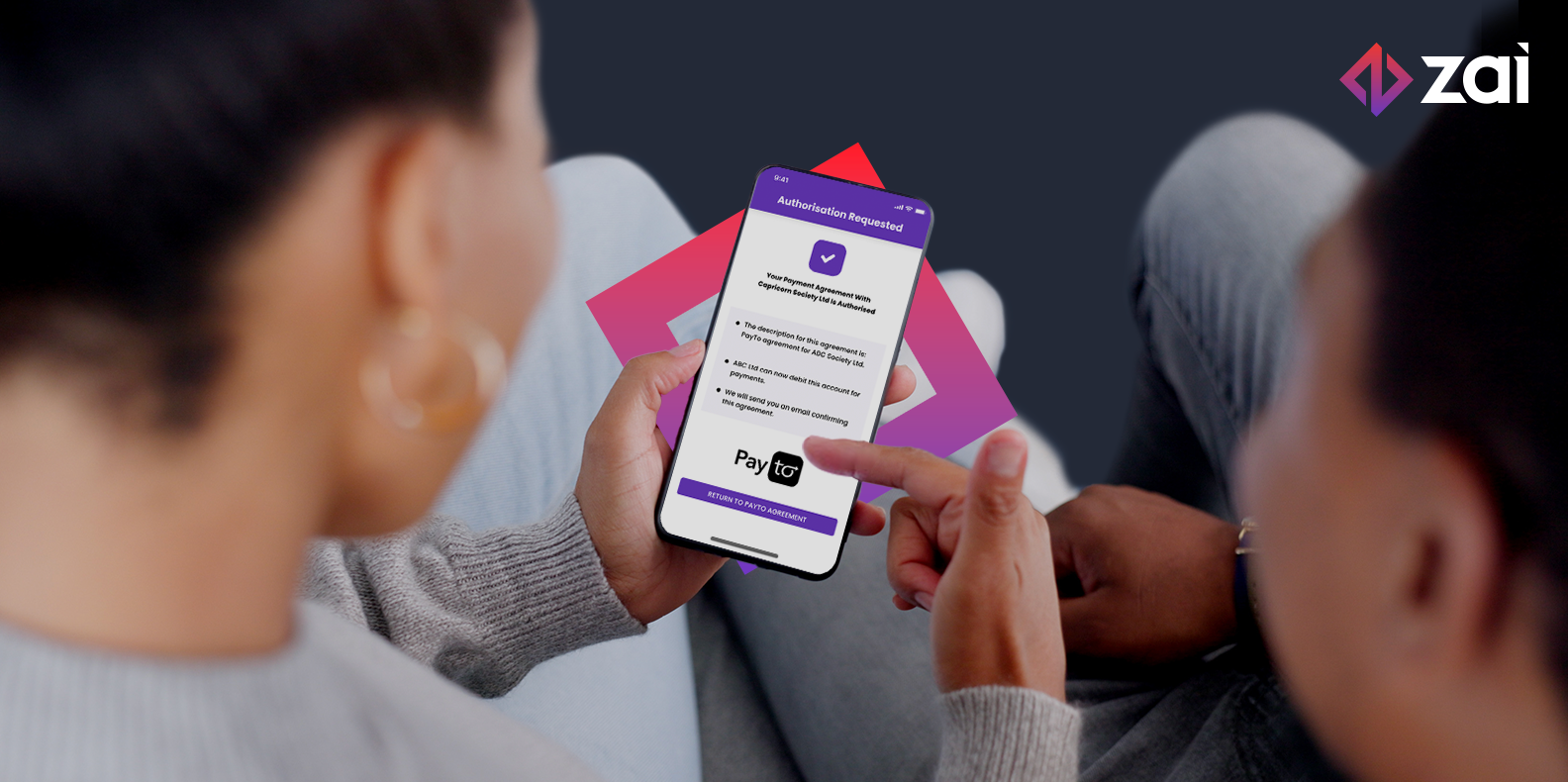

If a payer customer wants to set up a PayTo agreement they will need to provide information to the party they are establishing a PayTo agreement with (the merchant or biller, for example). They will then be presented with the PayTo agreement in their banking channel for them to authorise. We’ve worked on some CX guidelines and requirements to ensure some consistency in the PayTo customer experience, particularly for the authorisation process.

Once a PayTo agreement is authorised, the initiating party can send a payment initiation request to the financial institution holding the payer customer’s bank account requesting the payment to be made. Customers will see their PayTo agreements in their banking channel so they have visibility to what they have authorised and all of the specific details.

As part of the service, we have defined rules around what our participating organisations need to do in relation to the creation and maintenance of PayTo agreements and the processing of associated payments. This also includes rules around liability and fraud, returns and investigations.

What sectors are most likely to be interested in PayTo immediately upon launch?

That’s hard to say. We have seen significant interest in the market from a number of quarters including: merchants looking for alternative payment options for their customers; payment service providers wanting to provide better payment services; organisations wanting to offer their customers the choice of using their bank account as a funding source rather than just relying on cards; businesses seeing efficiency opportunities on the business-to-business (B2B) side such as being able to combine PayTo with e-Invoicing.

We see potential application for the PayTo service in almost every aspect of payments – whether that’s for consumer-to-business (C2B) payments, B2B or government payments. And that’s why we’re really excited about it – because we see it as being truly transformational.

How will you market and promote PayTo?

Our focus will be primarily on market educational type of activity – explaining to businesses that want to use the service and to payer customers – what it means for them, the benefits, how it works, addressing frequently asked questions – so really the “why” and the “how”. It will be up to individual providers to promote their own specific services that utilise PayTo.

What kind of uptake and volumes are you anticipating for PayTo in year one? Have you set yourselves targets?

We expect to see progressive take up of the service once the service is delivered to the market. We haven’t set ourselves any specific targets as ultimately we don’t really have control over volumes – that’s up to others in terms of how they want to use the service. But we’re certainly excited about the possibilities. Different organisations will move at various speeds – we anticipate seeing a number of early adopters looking to use the service and other organisations will need more time to make any system or process changes that may be required.

What other countries in the world are leading in the realm of real-time pull payments?

Whilst there is a lot of interest globally about real-time pull payments, it’s still a relatively new area. I would say India is probably leading the world.

Are you collaborating with them in any way to share information and build best-in-class functionality?

We’ve had discussions with a number of real-time payment system operators around the world to share learnings and best practices – and these discussions are always a really valuable source of information.

As each market is unique in terms of their infrastructure and specific market dynamics though, we’ve also made sure that we collaborated with potential users of the service and conducted user testing to ensure the service was tailored to the needs of Australian businesses and consumers.

You can read more about PayTo here.

PayTo is expected to roll out from mid-2022 onwards and Zai, as a payment initiator, will deliver a suite of best-in-class solutions including the management of mandates and the ability to initiate payment requests across sectors such as proptech, crypto and remitters. This will allow businesses to plug seamlessly into the PayTo service, providing their customers with a revolutionary new way to manage their payment arrangements.