.jpg?width=1065&height=534&name=fintech%20app_blog%20(2).jpg)

In 2021, 15 new Australian fintechs joined the payments sector, while the number of active fintechs in Australia increased from 701 to 718. These insights from KPMG show a steady growth in demand for Australian fintech.

However, securing a place of relevance and leadership in Australia’s booming fintech industry will require fintech companies to pay close attention to the shifting landscape of consumer expectations.

Fintechs looking to scale must also be at the cutting edge of payments technology. This means deploying the most effective payments workflow and providing automated solutions to existing and emerging challenges.

This article will unpack the nine features consumers expect from fintech payments in 2022, and consider the ways fintechs can improve their payment experience while gaining the agility required to scale.

1. Faster real-time payments

Many in the payments industry will use the terms “faster” and “real-time” interchangeably, but some fintechs may be falling short of consumer expectations.

In an on-demand culture, it’s increasingly difficult to justify delays in moving money, and 50% of consumers expect real-time payments to be instantaneous. When it comes to person-to-person (P2P) payment services, 70% of users expect funds to be received within the hour and 87% expect same-day delivery.

There are more than 90 Australian banks using the New Payments Platform (NPPA) and moving money within seconds. Enabling instant money movement is becoming a major differentiator in the market, and fintechs falling short of their claims risk falling behind the banks.

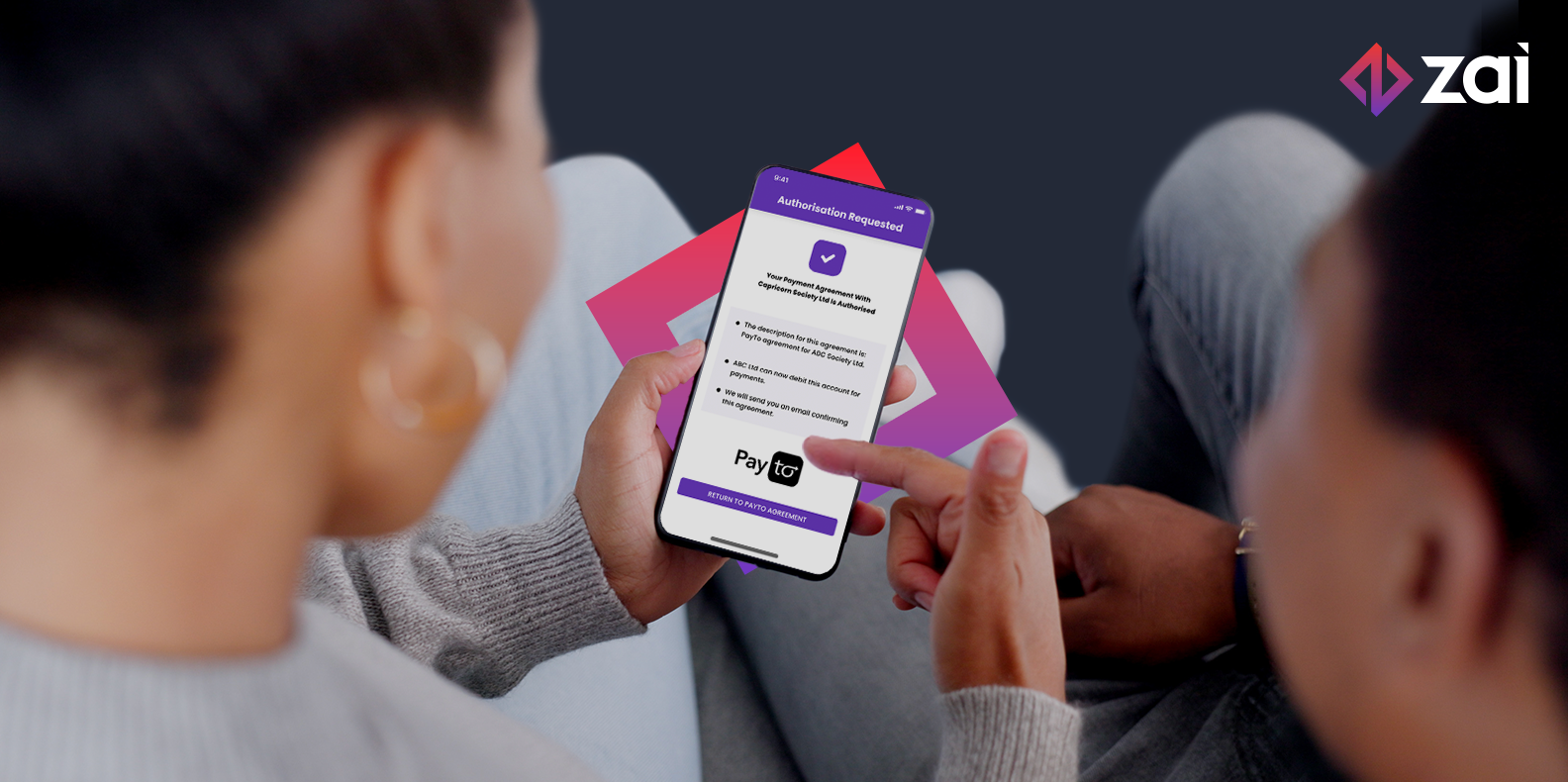

Zai sat down with Katrina Stuart from NPPA to discuss the upcoming launch of PayTo - a real-time payment service set to modernise the way bank accounts are used for payments, underpinning innovation in the sector for years to come. Katrina’s insights demonstrate Australia’s potential to become a global leader in real-time payments.

2. As little cost as possible

From merchant acquiring fees to currency exchange fees, making payments the traditional way isn’t cheap. According to EY research, attractive rates and fees have overtaken the ease of setting up an account as the primary reason consumers choose fintech over traditional financial services.

This insight indicates that fintech is now a mature market where low costs are the expected norm. Fintechs using blockchain technology could enable a further reduction in the cost of their payment services and stand out in the market.

3. Seamless self-service

When the world moved to remote-first in 2020, the rising need for a seamless self-service experience was seen across most industries. By 2022, even grandma expects DIY digital payments.

According to Fintech Alliance, roadblocks during the payment process permanently deter more than half of consumers when making transactions online. To optimise for self-service, fintechs must deploy intelligent data analysis to anticipate customer needs, predict potential roadblocks, and provide a clear path to resolution.

4. All-digital experiences, but human when needed

Fiserv’s 2021 research reveals that more consumers are choosing to manage their money through mobile than ever before. Although the payments industry is definitely trending towards self-service and digital-first, consumers like to know that human help is on hand when they need it.

It’s also important to consider the COVID-19 pandemic’s impact on consumer needs. Restrictions, lockdowns and the shift towards a remote, contactless, digital-only way of life have reduced opportunities to satisfy one of the most basic of human needs – connection.

To stand out in the industry, fintechs must tread a fine line between increased automation and maintaining a strong sense of human connection with consumers. Using Application Programming Interfaces (APIs) and plugins to simplify complex workflows can free up time to focus on customers and deliver the authenticity, empathy, and personality that fintech customers are craving.

5. Range of functionality

Having access to a range of functions and features is one of the top reasons consumers choose fintech over traditional banking. It’s also the number one factor driving fintech adoption among small and medium-sized enterprises (SMEs).

There are many services traditional financial institutions don’t provide, and consumers are turning to fintech to fill in the gaps. Fintechs with a range of tools and services from crypto to credit checks are able to provide consumers with a well-rounded financial experience.

60% of fintech users and 38% of non-users would prefer to view all of their financial products in one digital place. Beyond making payments, consumers want one platform for investing, saving, budgeting, accounting, financial advice and more.

Consolidated, multifunctional fintechs that manage all payment types on a single platform are better equipped to meet consumer expectations in 2022.

6. Availability of services 24/7

As 24/7 service removes the barriers to financial freedom for the on-demand consumer, waiting for “opening hours” to send and receive money is becoming a thing of the past.

Making services available 24/7 also enables fintechs to think global from the outset by diminishing the geographical barriers and time zone differences that might inhibit the company’s ability to scale.

Meeting this expectation requires considerable automation and integration, as well as the use of artificial intelligence (AI)-powered chatbots across multiple channels for round-the-clock customer service.

7. Ease in setting up, configuring and using

An easy set-up and configuration process is vital when it comes to attracting the curious consumers who are frustrated with their current financial experience. A frictionless set up means they can quickly solve their problem and shift their attention to their priorities.

However, making certain tasks slightly less easy than others lets the consumer know their money is in safe, trustworthy hands. While consumers have come to expect ease of use from fintechs, a platform experience that is too effortless can lead to users making costly mistakes with their money.

Increasing user friction for specific tasks is an important pillar of user experience (UX) design for fintechs. For example, a payment app should force the user to confirm their action before sending money. Consumers will thank their favourite fintech for a little friction where it counts!

8. High-level security

While Gen Z and millennials are far more inclined than older generations to share financial information with a fintech company, 71% of fintech users worry about the security of their personal data when dealing with companies online.

Since the technologies that enable greater convenience and usability also complicate the nature of consumer security, this concern isn’t exactly unwarranted. As the Australian fintech industry continues to boom and app-based traffic surges, storing data safely is an increasingly cumbersome task.

Fortunately, there are a number of ways to handle data safely and combat cyber crime:

Graduated identification

Not only does the collection and storage of personally identifiable information (PII) make consumers feel uneasy, but it’s also a major headache for fintechs attempting to scale.

Graduated identification processes are ideal for fintechs because they ensure end-users never provide more data than absolutely required.

Two-step authentication

Two-step authentication (also known as two-factor or multi-factor authentication or, by Google, as 2-step verification) is an additional layer of security over and above a basic password, usually in the form of a unique code sent to the user's mobile device.

A report by Fintech Alliance revealed that consumers are willing to pay a premium to boost their security through two-step authentication.

Blockchain technology

In addition to enabling fintechs to operate in a faster and cheaper way, blockchain technology also comes with a much lower error rate with fewer resulting risks, lower capital requirement and less vulnerability to cyber attacks.

9. Payments across borders

While low-cost, self-service, real-time domestic payments have become the new normal, payments across borders are next on the fintech agenda. As there is no single system that connects various banks all over the world, sending money internationally has been a challenging, slow and expensive process for consumers.

According to The Economic Times, the average cost worldwide of sending US$200 stood at 6.38% during the first quarter of 2021.

Sending money across borders and currencies reveals the greatest inefficiencies, delays and lack of transparency in the payments industry today. However, the technology available in 2022 sets the stage for Australian fintechs to revolutionise international payments and usher in a new level of consumer expectations.

To scale with agility and secure a place of relevance and leadership in Australia’s booming fintech industry, CEOs must put their customer experience at the top of their agendas and ensure their chief product or technical officer has these nine user expectations baked into their roadmap.

This information is correct and updated as of February 2022. This information is not to be relied on in making a decision with regard to an investment. We strongly recommend that you obtain independent financial advice before making any form of investment or significant financial transaction. This article is purely for general information purposes.