Real-time payments are set to undergo a revolution in Australia with the introduction of PayTo. Previously known as the Mandated Payments Service (MPS), PayTo is the latest initiative from the New Payments Platform Australia (NPP), responsible for delivering instant, real-time payments for all types of businesses and their customers since 2018.

What is PayTo?

PayTo is an innovative digital payment system from the New Payments Platform Australia (NPP) and Australia’s financial services industry. It enables businesses to initiate recurring or ad-hoc real-time payments from their customers' bank accounts.

How does PayTo work?

PayTo is built on the NPP’s payments infrastructure of real-time payment rails.

Businesses can set up a PayTo agreement with customers who can authorise the details, including the amount and date of a recurring payment (or date of purchase for one-off payments).

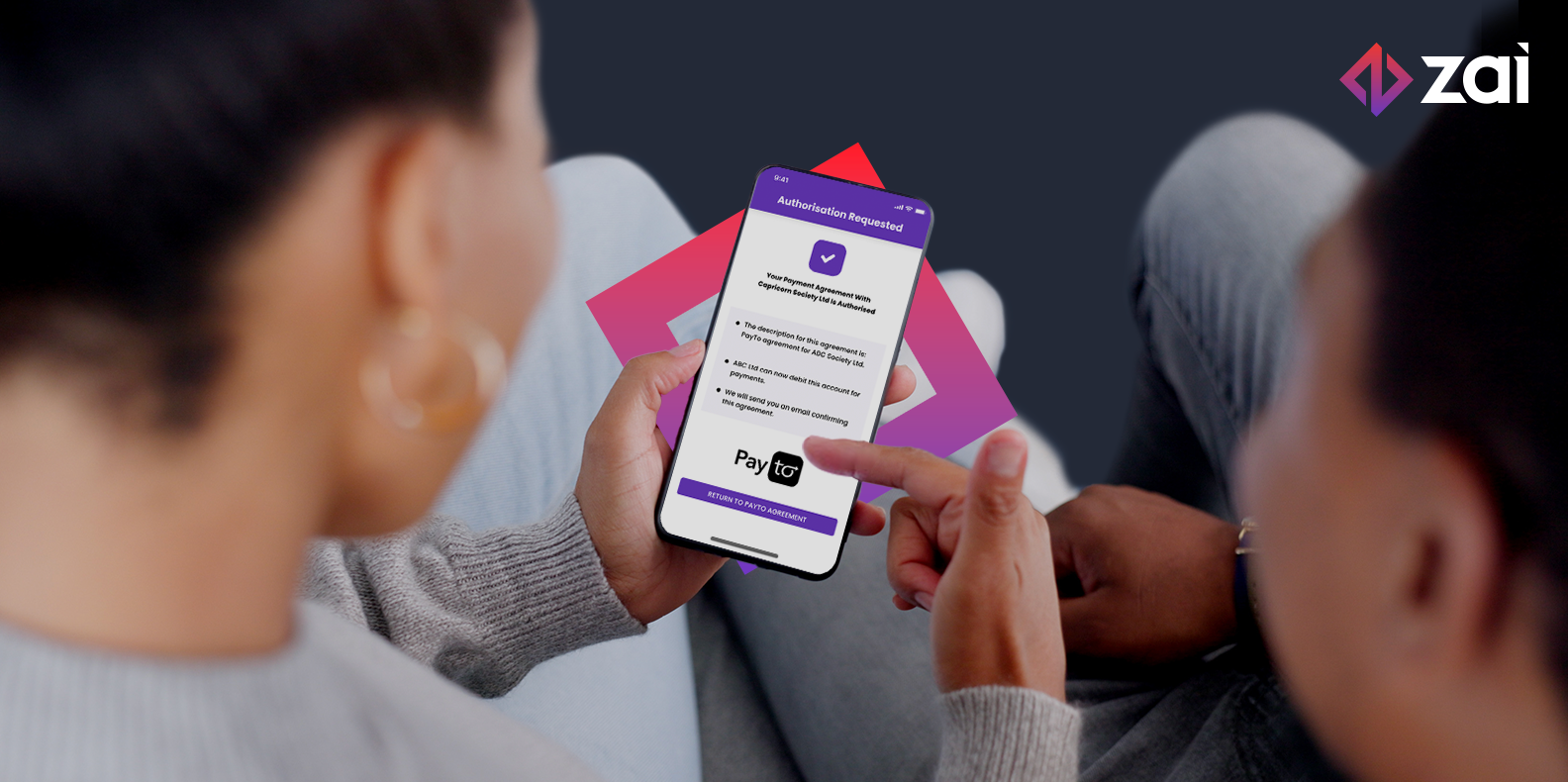

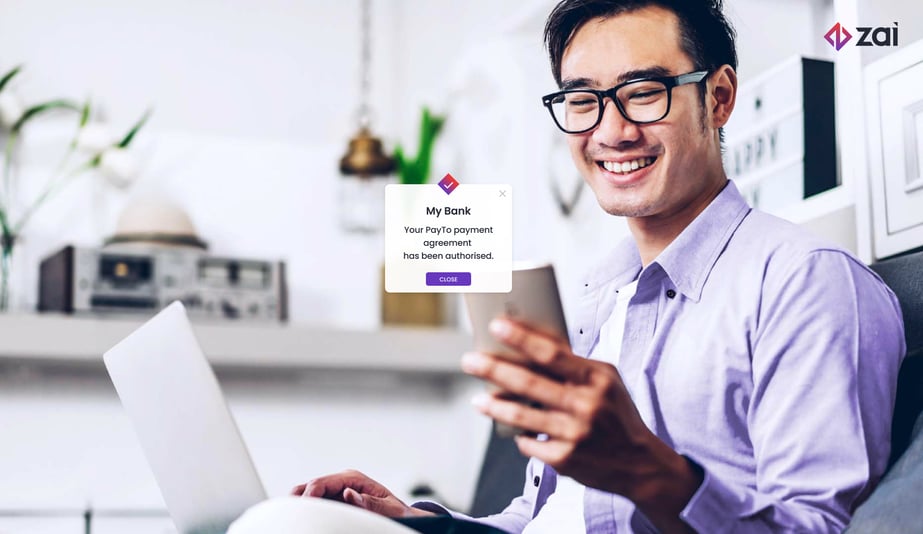

The PayTo agreement appears in the customer’s online banking system, financial institution account or mobile banking app so the customer can digitally approve and activate the agreement. As a mandated agreement, the business can automatically debit a customer’s account according to the contracted conditions.

Push vs pull payments

To understand how PayTo works, it’s essential to know the difference between “pull” payments and “push” payments. As the name suggests, a push payment is when the customer has to initiate a payment from their bank account to a company or service provider, pushed out by the payer customer. A pull payment is a transaction initiated by a payee, pulled in by the company or service provider.

PayTo is a pull payment. As soon as the customer authorises an agreement set up by the merchant or payee, payments (whether one-off or recurring) occur automatically once the company requests payment initiation.

Until PayTo, the NPP has only offered push payments where the payee triggers the payment from their account via their banking channel. However, that will change as PayTo rolls out, enabling customers to authorise a third-party to initiate payment via the NPP.

What makes PayTo different?

As a new way to pre-authorise digital payments, PayTo is a way for businesses to initiate real-time payments from their customers’ bank accounts. It’s a relatively simple concept, but its impact will be far-reaching because PayTo offers greater functionality than legacy payment methods, such as direct debits. Payments will be more efficient and less complicated for businesses and customers alike.

PayTo vs direct debits

PayTo and direct debit payments share similarities. They are both mandated agreements and pull payments, so it’s easy to think they’re the same system.

However, there are key differences between the two:

-

Processing times. PayTo payments can arrive in less than 60 seconds. Direct debits can take up to three business days.

-

Authentication. PayTo provides real-time account validation, whereas validity of accounts through direct debits remains uncertain.

-

Payment data. Direct debits contain limited data on each transaction, meaning the customer may not understand (or remember) the reason for payment. PayTo is detail rich, so your customers will always have a clear overview of their transactions with you.

-

Authorisation. PayTo offers real-time digital authorisation and is completely paper free. Direct debits rely on paper-based mandates or online forms (which need to be printed or stored digitally) making authorisation slow and unclear.

-

Notification. Changes to direct debits are difficult to trace. PayTo provides both parties with real-time notifications of changes, interruptions or cancellations.

Why use PayTo?

PayTo builds on all the useful features introduced with the NPP platform and provides numerous reasons for wide adoption:

-

Speed. Payments clear and settle in less than 60 seconds.

-

Always-on technology. Around-the-clock availability, 365 days per year.

-

Greater transparency. Enriched descriptions that furnish better payment information for easier reconciliation.

-

Seamless customer experience. PayID – an easy-to-remember unique identifier, such as an email address or Australian business number (ABN) – can be used to direct and accept PayTo payments.

-

Flexibility. Endless range of use cases, from traditional marketplace purchases to e-invoicing, accounts payable, one-off e-commerce transactions, and QR code payments.

-

Agility. No paperwork needed like direct debits. PayTo mandates can be set up quickly and easily.

Now, setting up a payment will be more convenient and transparent, improving the payments experience for customers and offering additional benefits for businesses.

PayTo for businesses

With PayTo, merchants and businesses can now initiate real-time payments (one-off or recurring) in varying amounts, directly from customer bank accounts.

PayTo removes payment uncertainty because account validation and fund verification are already built in. Businesses will also have full visibility when a payment agreement is paused, cancelled or altered.

PayTo means instant payments. Transactions, such as direct debits, that would normally take 2 to 3 business days through the Bulk Electronic Clearing System (BECS) are now processed in real-time.

PayTo is secure and protects against fraud. Customer and account verification takes place in real-time within the process. This means less administration, a reduced need to troubleshoot payment status, and automatic reconciliations.

A cost-effective and more efficient alternative to cards. With PayTo, you’ll no longer have the heavy merchant processing fees that come with accepting credit cards. In addition, PayTo provides:

-

Assurance of funds with real-time verification of accounts and fund availability.

-

24/7 processing so you can avoid waiting days for the payment information to update in your banking portal.

-

Autonomous time limits. The participating parties can determine the duration of the mandate, without being subject to a credit card expiry date.

PayTo for customers

Customers will have more control and visibility over payments coming out of their bank account with PayTo.

PayTo offers more convenience and less work for the customer. Whether it’s for a subscription, a cryptocurrency transaction or rental payments, customers can set up a PayTo agreement from their banking app quickly. Customers can also authorise, pause or cancel agreements when necessary with a click.

Customers will have full visibility over payments thanks to enhanced payment information.

As an entirely digital payment option, PayTo is data-rich and consists of digital payment arrangements (mandates) so customers can view and change their agreement online and in-app at any time.

PayTo & Zai: Get started today

PayTo is set to be a game-changer for the Australian payments industry, marketplaces and online platforms thanks to its convenience, efficiency and security. Industries such as fintechs, property management companies, online marketplaces and any business looking to streamline their payment processes will be able to move money more smoothly through their operations.

APIs will be central to making PayTo work seamlessly for businesses. This means Zai can help you prepare for and integrate this revolutionary payment option. We can help manage your mandate and help you initiate payments seamlessly, offering more flexibility, certainty and transparency to you and your customers.

For more information on PayTo and payment solutions that work for your business, get in touch with us today.